2026 Housing Market Forecast: Will The Market Finds Its Footing On Prices, Rates, And Demand

2026 US Housing Market Forecast: Will the Market Find Its Footing?

Will 2026 finally be the year that homebuyers stop waiting on the sidelines? Leading housing forecasters are sharply divided, projecting anywhere from 1.7%¹ to 14%² growth in home sales. That 12-point spread highlights the core issue facing the U.S. housing market: to what extent will slightly lower mortgage rates and the gradual erosion of the lock-in effect actually release pent-up demand?

Nearly every major forecasting organization agrees that the housing market in 2026 will be more active than in 2025. Beyond that shared outlook, however, expectations diverge significantly regarding both the pace and scale of recovery. The National Association of Realtors projects a robust 14% increase in sales activity, while Realtor.com anticipates only a modest 1.7% improvement. In reality, both outcomes could prove accurate depending on region, price tier, and local economic conditions.

Nearly every major forecasting organization agrees that the housing market in 2026 will be more active than in 2025. Beyond that shared outlook, however, expectations diverge significantly regarding both the pace and scale of recovery. The National Association of Realtors projects a robust 14% increase in sales activity, while Realtor.com anticipates only a modest 1.7% improvement. In reality, both outcomes could prove accurate depending on region, price tier, and local economic conditions.

For buyers, sellers, and homeowners tracking equity performance, these conflicting forecasts matter less than the underlying market fundamentals. Mortgage rates are expected to decline slightly. Inventory should continue its gradual improvement. Home prices will likely keep rising, though at a slower and more sustainable pace. The broader trend suggests a market in the process of thawing after the extreme distortions of the pandemic years. More importantly, housing appears to be transitioning back toward the steadier rhythm of historical norms. There are reasons to be optimistic about the 2026 housing market.

The 2025 Context: Why the Market Stayed Frozen

The housing market of 2025 largely underperformed expectations. Mortgage rates remained stubbornly above 6.5%, suppressing demand and keeping transaction volumes near historic lows.⁸ By mid-2025, more than 80% of U.S. homeowners held mortgage rates below 6%, reinforcing the lock-in effect that discouraged potential sellers from entering the market.³

Affordability challenges intensified. The median age of first-time homebuyers rose to 40 years old⁴, reflecting how elevated home prices and higher borrowing costs placed ownership increasingly out of reach for younger households. While the market avoided a crash, it failed to meaningfully recover, with transaction volume remaining constrained and mobility limited.

2026 Predictions: Where Forecasters Agree and Disagree

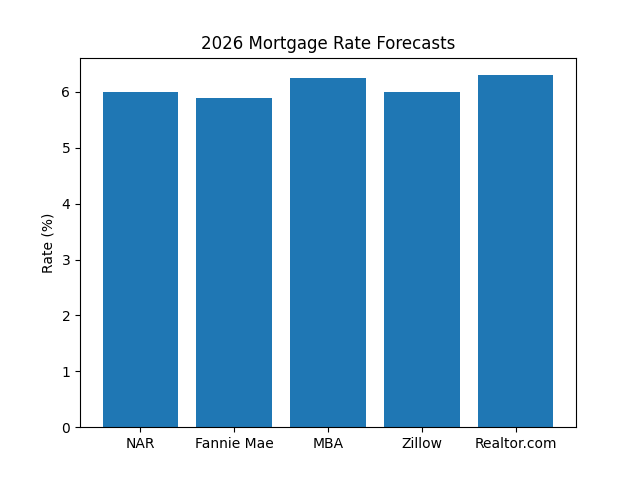

Mortgage Rates: Broad Consensus on Modest Improvement

Housing economists largely agree on the expected path of mortgage rates in 2026. Forecasts cluster tightly within the 6.0% to 6.4% range, representing modest but meaningful improvement compared with 2025.

The critical question is whether this decline will meaningfully stimulate activity. A drop from 7% to 6.5% may not move buyers who are still hoping for a return to 5% rates, nor sellers locked into 3% mortgages. The National Association of Realtors estimates that a decline to 6% could unlock 5.5 million additional buyers, including 1.6 million renters.² Yet forecasters’ sharply different sales projections reflect uncertainty about how powerful this effect will be in practice.

Existing Home Sales: The Primary Wild Card

Forecasts for existing home sales in 2026 vary far more than interest-rate projections, reflecting divergent assumptions about how quickly consumer behavior will normalize.

The range from 1.7% to 14% growth illustrates genuine uncertainty about buyer and seller psychology. Will homeowners with ultra-low mortgages finally accept that 6% represents the new baseline? Will life events such as career changes, family needs, relocations, or divorce ultimately outweigh the financial cost of surrendering cheap debt?

Several forces must align. The lock-in effect must continue to weaken. As more homeowners reach the point where life circumstances outweigh rate advantages, mobility should increase. Buyers must also psychologically shift away from waiting for pandemic-era rates and accept the current environment as normal. With 6%–7% now firmly established and further declines expected, many buyers may re-enter the market.

Employment and income stability remain fundamental. Continued job growth and wage increases provide the financial foundation for both buyers and sellers. Several forecasters expect slowing price growth combined with rising incomes to gradually improve affordability in 2026.¹ Conversely, any deterioration in labor markets would push results toward the lower end of projections.

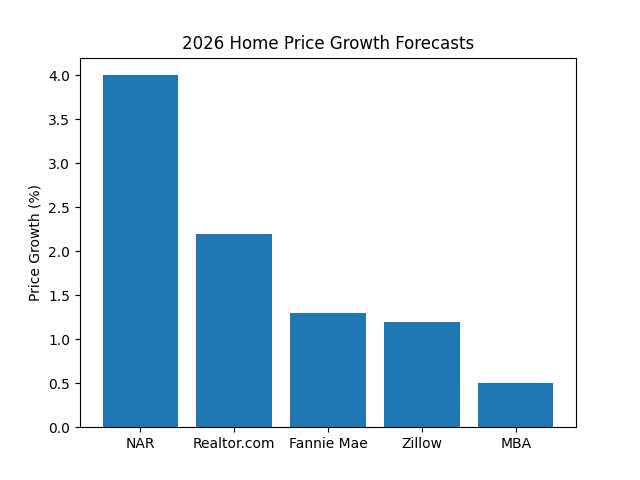

Home Prices: Continued Appreciation, Slower Pace

All major housing forecasters expect home prices to continue rising in 2026, though growth rates are projected to be far more restrained than during the pandemic boom.

Based on Q2 2025 median price of $410,800

Compared with the uncertainty surrounding sales volume, price forecasts cluster relatively tightly. Supply-demand fundamentals continue to support prices, even as transaction volumes remain subdued. Inventory remains below the level associated with a balanced market after years of underbuilding relative to household formation. Existing homeowners hold substantial equity, limiting forced sales and allowing many move-up buyers to deploy equity toward new purchases.

Projected appreciation reflects a return to historically typical growth rates rather than the extraordinary gains of recent years.

What This Means for Buyers

For buyers, 2026 requires balancing affordability constraints against the recognition that waiting may not produce significantly better conditions. However, experts are forecasting improvements in affordability in 2026.

For buyers, 2026 requires balancing affordability constraints against the recognition that waiting may not produce significantly better conditions. However, experts are forecasting improvements in affordability in 2026.

Accepting the New Rate Reality

Mortgage rates in 2026 are expected to settle in the 6.0%–6.4% range. Rates below 3% were products of emergency monetary policy and are unlikely to return soon. Buyers waiting for 4%–5% may need to recalibrate expectations. Planning around current levels while retaining the option to refinance later provides a more realistic framework.

Improved Supply and Buyer Leverage

Inventory has improved compared with recent years, providing buyers more options and negotiating flexibility.¹ Days on market have lengthened, bidding wars are less common, and sellers are more open to contingencies, repairs, and concessions.⁵ Well-priced homes in prime locations still command attention, but overall conditions are far more balanced than during the pandemic surge.

Pricing and Competition Dynamics

Prices are projected to rise modestly, meaning waiting is unlikely to deliver meaningful discounts. However, slower appreciation reduces urgency and allows buyers to be selective. Overpriced listings face greater resistance as buyers gain more alternatives.

First-Time Buyer Challenges

First-time buyers remain under the greatest pressure. The median age of 40⁴ underscores the difficulty of entering homeownership amid high prices and rates. While modest improvements may ease conditions slightly compared with 2025, affordability remains a significant barrier. Creative strategies, assistance programs, and targeting more affordable markets remain essential tools.

What This Means for Sellers

For sellers, 2026 remains favorable, but leverage is no longer universal. Outcomes depend heavily on pricing accuracy, location, and property condition.

For sellers, 2026 remains favorable, but leverage is no longer universal. Outcomes depend heavily on pricing accuracy, location, and property condition.

Evaluating the Mortgage Rate Trade-Off

While the lock-in effect persists, many owners now possess significant equity that offsets higher borrowing costs. Life events increasingly outweigh rate considerations as sellers adapt to the new environment.

Pricing Strategy

Overpricing risks extended market time and eventual reductions. Buyers are patient, informed, and equipped with more options. Homes priced correctly from the start perform best.

Concessions as a Strategic Tool

Closing cost credits, rate buydowns, and repair allowances have become standard tools for bridging affordability gaps without slashing list prices.

Preparation and Presentation

With rising inventory, presentation once again drives outcomes. Minor improvements and professional staging significantly influence buyer perception and final pricing.

What This Means for Renters

Renting in 2026 remains a rational choice for many households. While rent growth has slowed, ownership costs remain high. The rent-versus-buy decision depends on location, finances, and time horizon. For renters aiming to buy, 2026 offers an ideal preparation period for strengthening finances and positioning for future opportunity.

Conclusion: A Market in Transition

The 2026 housing market is defined by normalization rather than disruption. Rates stabilize in the low-to-mid 6% range. Sales activity gradually improves. Prices rise at sustainable historical levels. Success in this environment depends less on timing and more on realistic expectations, financial readiness, and alignment with personal circumstances.

If you’re considering buying or selling a home in the Greater Charlotte area in 2026, understanding how national housing trends intersect with local market realities is essential. Charlotte’s housing market continues to be shaped by population growth, employment expansion, neighborhood-specific demand, and shifting affordability conditions that do not always reflect national averages. Nina Hollander, Coldwell Banker Realty, has been guiding Charlotte-area buyers and sellers since 1999 and brings more than three decades of market knowledge, strategic insight, and hands-on experience to every transaction. Whether you’re planning your next move or simply evaluating your options, reach out to me for informed, personalized guidance to help you navigate the 2026 market with confidence and clarity.

References

-

Realtor.com

https://www.realtor.com/news/trends/housing-forecast-2026-mortgage-rates-affordability-improves/ -

NAR Real Estate Forecast Summit

https://www.nar.realtor/events/nar-real-estate-forecast-summit -

RealtorMag

https://www.realtor.com/news/trends/mortgage-rates-below-6-percent-august-2025/ -

National Association of Realtors (NAR). (2025, November). First-Time Home Buyer Share Falls to Historic Low of 21%, Median Age Rises to 40.

https://www.nar.realtor/newsroom/first-time-home-buyer-share-falls-to-historic-low-of-21-median-age-rises-to-40 -

Zillow

https://www.zillow.com/research/2026-housing-predictions-35800/ -

NAR

https://www.nar.realtor/sites/default/files/2025-11/ehs-10-2025-summary-2025-11-20.pdf

Thinking about buying or selling a home in the Charlotte area?

Nina Hollander is an expert local real estate agent serving Charlotte and surrounding communities. Whether you’re just starting your search or ready to make a move, Nina is here to provide trusted guidance every step of the way. Contact Nina today to get personalized help with your real estate goals.

Thinking about selling your Charlotte home? Request our free Charlotte home value report and to see what your home may be worth in today’s real estate market.

Check out the Real Estate Market in Charlotte NC

I work hard for my clients to ensure they have the best selling or buying experience possible. For comprehensive real estate information in the Greater Charlotte NC area, check out the links below!